728x90

반응형

SMALL

데이터셋 로드

Medical_Insurance_dataset.csv

0.22MB

import pandas as pd

df = pd.read_csv('Medical_Insurance_dataset.csv')

df.head()

원-핫 인코딩

df = pd.get_dummies(df)

df.head()

데이터 전처리

# 훈련 데이터, 검증 데이터, 테스트 데이터 나누기

features = df[df.keys().drop('charges')].values

outcome = df['charges'].values.reshape(-1, 1)

from sklearn.model_selection import train_test_split

train_features, test_features, train_target, test_target = train_test_split(features, outcome, test_size=0.3)

train_features, val_features, train_target, val_target = train_test_split(train_features, train_target, test_size=0.3)

데이터 스케일링

from sklearn.preprocessing import MinMaxScaler

feature_scaler = MinMaxScaler()

train_features_scaled = feature_scaler.fit_transform(train_features)

val_features_scaled = feature_scaler.transform(val_features)

test_features_scaled = feature_scaler.transform(test_features)

모델 훈련

from xgboost import XGBRegressor

from xgboost.callback import EarlyStopping

xgb = XGBRegressor()

early_stop = EarlyStopping(rounds=20,metric_name='rmse',data_name="validation_0",save_best=True)

xgb.fit(train_features_scaled, train_target,eval_set=[(val_features_scaled, val_target)], eval_metric='rmse', callbacks=[early_stop])

result = xgb.predict(test_features_scaled)# 회귀 성능 평가

from sklearn.metrics import mean_absolute_error, mean_squared_error

import numpy as np

print('MAE :',mean_absolute_error(test_target, result))

print('RMSE :',np.sqrt(mean_squared_error(test_target, result)))MAE : 1778.4481490093838

RMSE : 3678.061753847381import matplotlib.pyplot as plt

%matplotlib inline

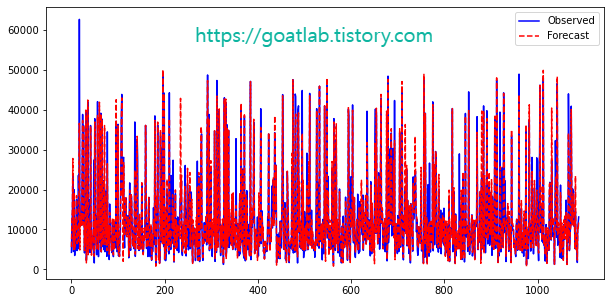

plt.figure(figsize=(10,5))

plt.plot(test_target,linestyle='-',color='blue',label='Observed')

plt.plot(result,linestyle='--',color='red',label='Forecast')

plt.legend()

plt.show()

GridSearchCV를 통한 최적화

from xgboost import XGBRegressor

from sklearn.model_selection import GridSearchCV

xgb = XGBRegressor()

parameters = {'learning_rate':[0.01,0.05,0.07,0.1]}

xgb_grid = GridSearchCV(xgb, parameters, cv = 5, n_jobs=-1)

xgb_grid.fit(train_features_scaled,train_target)# 하이퍼파라미터 최적화

print(xgb_grid.best_score_)

print(xgb_grid.best_params_)0.8931528352067961

{'learning_rate': 0.07}# 최적의 하이퍼파라미터를 설정하고 학습

from xgboost import XGBRegressor

from xgboost.callback import EarlyStopping

xgb = XGBRegressor(learning_rate=0.05)

early_stop = EarlyStopping(rounds=20,metric_name='rmse',data_name="validation_0",save_best=True)

xgb.fit(train_features_scaled, train_target,eval_set=[(val_features_scaled, val_target)], eval_metric='rmse', callbacks=[early_stop])

result = xgb.predict(test_features_scaled)# 성능 평가 결과

from sklearn.metrics import mean_absolute_error, mean_squared_error

import numpy as np

print('MAE :',mean_absolute_error(test_target, result))

print('RMSE :',np.sqrt(mean_squared_error(test_target, result)))plt.figure(figsize=(10,5))

plt.plot(test_target,linestyle='-',color='blue',label='Observed')

plt.plot(result,linestyle='--',color='red',label='Forecast')

plt.legend()

plt.show()

728x90

반응형

LIST

'Learning-driven Methodology > ML (Machine Learning)' 카테고리의 다른 글

| [Machine Learning] 이상 탐지 (Anomaly Detection) (0) | 2022.11.17 |

|---|---|

| [Machine Learning] 오토인코더 (Autoencoder) (0) | 2022.11.11 |

| [XGBoost] 심혈관 질환 예측 (0) | 2022.10.05 |

| [XGBoost] 심장 질환 예측 (0) | 2022.10.04 |

| [XGBoost] 위스콘신 유방암 데이터 (3) (0) | 2022.10.04 |